APAC: Mobile Payments, Checkouts & Wallet Innovation

Same Traffic, Same Offer… So What Changed?

You’ve probably seen this before. You take a campaign that works perfectly in one region, launch it in APAC… and suddenly, performance drops. The same offer, the same creatives, the same funnel structure, and often, even similar targeting logic.

Sometimes the change is small, but other times, it’s big enough to break your numbers. The first instinct is usually to blame the traffic, the audience, or the cultural differences.

And yes, those factors do matter…

However, what if the real issue shows up at the very end of your funnel?

Sit back, relax, and let’s talk about payment methods.

Payment as a Behavioral Layer

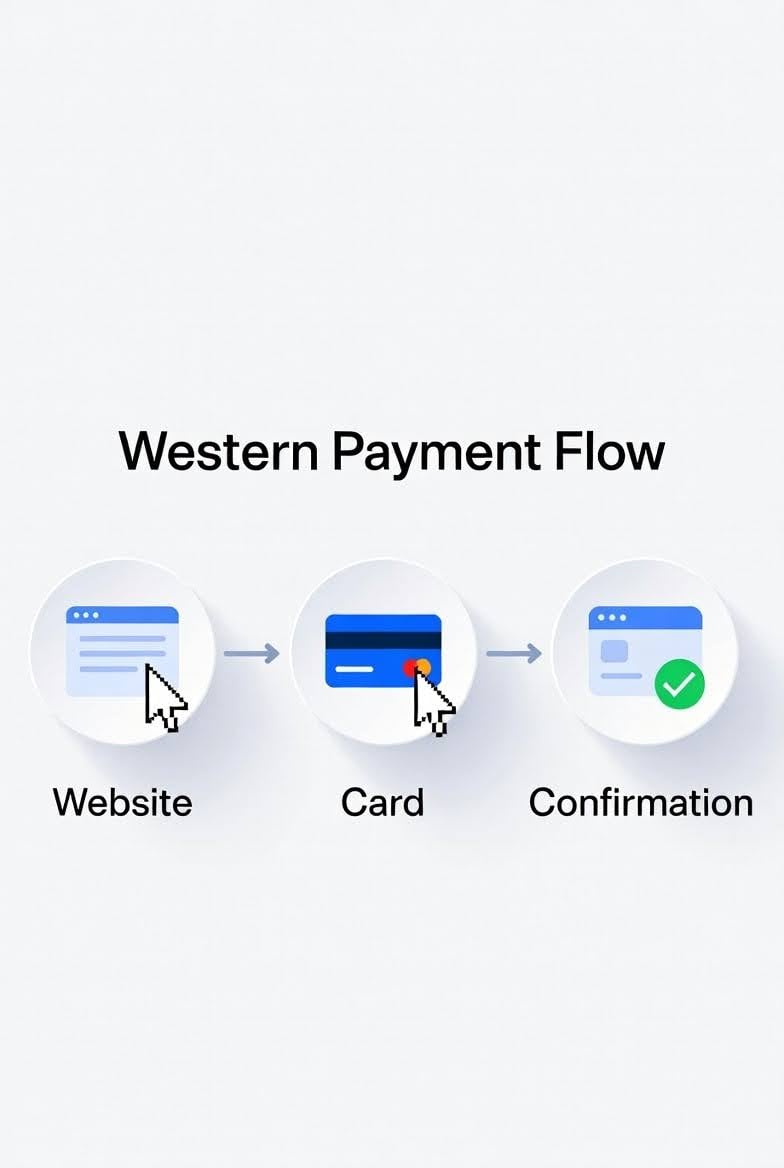

In many Western markets, payment is treated as a technical endpoint rather than a behavioral component, which is understandable given how standardized the experience has become. Users are used to entering their card details, confirming the payment, and completing the purchase in just a few steps. It’s a familiar process, so it rarely gets much attention when analyzing performance.

However, this logic doesn’t really apply to APAC. Here, payment is not just a final step. It’s part of a broader digital behavior, shaped by mobile-first ecosystems and deeply integrated financial tools.

What appears to be a minor implementation detail from a system perspective often represents a fundamental mismatch from a user perspective.

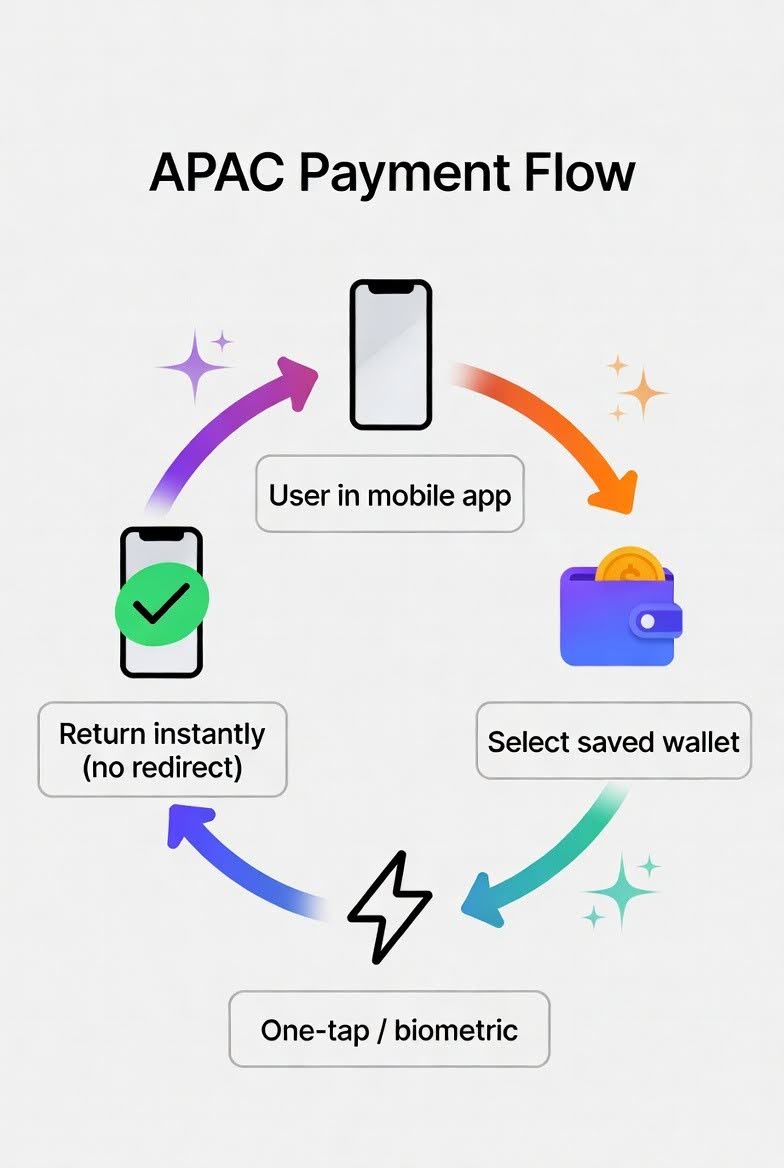

How Payment Behavior Differs in APAC

Across many APAC countries, payments don’t really revolve around cards. Instead, users rely on wallets, real-time transfers, and mobile-first interactions. These are not separate steps but mobile-native interactions that are built into what users already do every day.

Widely used payment solutions in APAC include:

- GCash (PH) – used for everyday payments, transfers, and services

- GrabPay (SEA) – built into the Grab ecosystem (rides, food, payments)

- MoMo (VN) – a go-to wallet for daily transactions

- OVO & GoPay (ID) – common for both online and offline payments

- UPI (IN) – allows instant bank transfers without cards (directly between accounts)

For many users, these are not “alternative”, but default payment methods. For this reason, user expectations are different. Payments are expected to be instant, familiar, and fully integrated into the apps they already use. It may look like a simple difference (cards vs wallets), but it actually reflects how users are used to paying.

In Western markets, users tend to trust the website. Entering card details feels like a natural step of the user’s conversion journey.

In APAC, trust is placed in the wallet or app first. That’s why users expect to complete payments inside that environment (rather than through an external checkout).

This distinction influences not only how users pay but also how they evaluate whether a transaction feels safe or convenient, and therefore, worth completing.

Where Conversion Begins to Break

When a card-based checkout meets a wallet-first audience, there’s a mismatch. Users don’t always reject it directly, but friction does appear (and many simply choose to leave).

A user arriving at a payment page in the Philippines, Indonesia, or Vietnam may instinctively look for familiar options such as GCash or GrabPay. If those options are not visible right away, the user starts hesitating. In practice, this moment looks like:

- The user scans the available payment methods and does not recognize their familiar option

- A short pause occurs, during which trust is no longer reinforced

- The user decides not to proceed, without attempting alternative methods

This behavior is not random. A foundational concept that helps explain it is the Mere Exposure Effect, first described by Robert Zajonc in 1968, which shows that people tend to develop a preference for things simply because they are familiar with them. In the context of payments, familiarity is not just a comfort factor – it directly influences perceived trust and the likelihood of action.

This hesitation rarely translates into feedback or measurable error signals, which is precisely why it is often overlooked, yet its impact on conversion can be substantial.

The relationship between payment and performance can be expressed in a way that parallels how we think about traffic context:

Conversion = Offer x Payment Fit

In simple words, a strong offer won’t save you if the payment method feels wrong. If friction appears exactly where conversion should happen, we have a problem, Houston.

Where APAC Payment Systems Are Advancing Faster

Beyond differences in adoption, APAC markets are also leading in several areas of payment innovation that are gradually reshaping user expectations globally. Take WeChat (CN) or Grab (SEA) as an example: these are not just apps – they’re ecosystems. You can chat, order food, book rides, and pay – all in one place.

So payment is not a separate step; it just happens inside what the user is already doing.

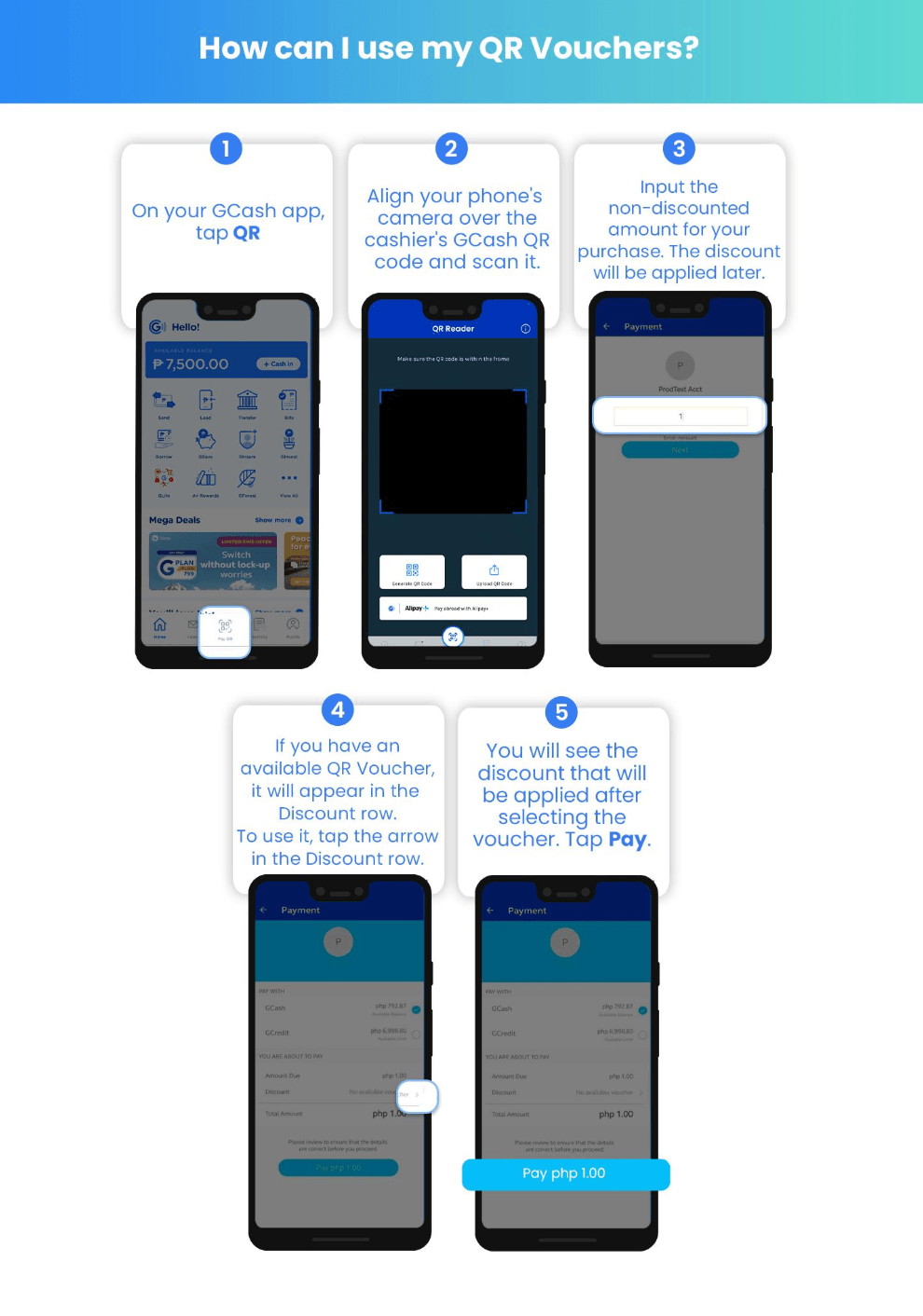

QR payments make things faster because users don’t need to enter card details – they just scan and pay. Smaller, more frequent payments are also very common. Instead of committing to one big purchase, users pay in smaller amounts over time, making them feel less committed.

Additionally, gamification elements such as rewards, cashback, and incentive systems have transformed payment from a purely functional action into part of an ongoing engagement loop.

Take a look at the examples below:

GrabPay

- GrabRewards points after each payment

- Discount vouchers (e.g., food, rides)

- Limited-time promos like “Pay with GrabPay and get 20% off”

GCash

- Instant cashback after paying bills or services

- Promo banners like “Pay now and get ₱50 back”

- In-app vouchers and seasonal campaigns

Alipay / WeChat Pay

- “Red packets” (hongbao) – random cash rewards

- Gamified campaigns (spin, collect, unlock rewards)

- Payment-linked bonuses during holidays or events

Adapting to APAC markets requires more than simply adding additional payment options; it involves rethinking how payment is presented, prioritized, and integrated into the user experience.

An effective approach to do so, would include:

- placing locally dominant payment methods at the forefront rather than treating them as secondary options

- minimizing the number of steps required to complete a transaction

- designing interfaces that reflect mobile-native interaction patterns rather than desktop-oriented forms

- incorporating recognizable visual elements associated with trusted local payment brands

- allowing for lower initial commitments through smaller transaction amounts

EXPERT VIEW: How does payment familiarity increase conversion rate?

Questions answered by MaxJmax, Performance Marketer in China

Q: Which local payment methods are typically enabled via PSPs but not shown to users upfront?

A: In many cases, local payment methods like bank transfers, e-wallets, or credit cards are enabled via PSPs but not shown upfront.

Q: How does wallet visibility impact CR? Is there a noticeable difference between showing them upfront vs hiding them within the checkout?

A: From what I’ve seen, showing key payment options upfront usually improves trust and reduces friction. But as long as the user wants to pay for the service/product, they will figure it out. The main reason that impacts CR is that some users want to pay but can’t.

Q: Which local wallets or payment methods are critical to display before the click to avoid losing conversions?

A: For example, in China, people like to see if it supports Alipay or WeChat Pay.

Q: Are there cases where adding local payment methods (such as GCash, UPI, or similar solutions) led to a significant increase in CR? What factors contributed to this uplift?

A: Definitely! Trust, convenience, and higher payment success rates.

Q: How much conversion are we potentially losing in APAC by relying only on global payment methods (cards, PayPal, etc.) without visible local options?

A: While the exact number varies by market, I would estimate the potential loss could be around 20–30%.

Practical Framework: How to Make Your Offer Asia-Friendly

Final Thoughts

Users would naturally rather rely on what they already know, what they have used before, and what feels immediately recognizable within the interface. When that recognition is present, trust follows naturally. When it is absent, hesitation appears – often quietly, without explicit signals (with a measurable, negative impact on conversion).

As a result, optimizing for APAC requires a shift in perspective. We are not speaking only about expanding payment coverage, but also about aligning the entire checkout experience with local expectations.

At the end of the day, conversion does not happen only when a payment method is available, but when it feels familiar.

Join our Telegram for more insights and share your ideas with fellow-affiliates!

Trends

View more posts